What is CBAM: The EU importers's guide to the Carbon Border Adjustment Mechanism

Disclaimer: New EUDR developments - December 2025

In November 2025, the European Parliament and Council backed key changes to the EU Deforestation Regulation (EUDR), including a 12‑month enforcement delay and simplified obligations based on company size and supply chain role.

Key changes proposed:

- New enforcement timeline: 30 December 2026 for large/medium operators, 30 June 2027 for small/micro operators

- Simplified DDS: One-time declarations for small and micro primary producers

- Narrowed scope: Most downstream actors and non‑SME traders would no longer need to submit DDSs

- New DDS requirement: Estimated annual quantity of regulated products must be included

These updates are not yet legally binding. A final text will be confirmed through trilogue negotiations and formal publication in the EU’s Official Journal. Until then, the current EUDR regulation and deadlines remain in force.

We continue to monitor developments and will update all guidance as the final law is adopted.

Key takeaways:

- CBAM introduces a carbon price on imported goods, with reporting already required and certificate payments starting from 1 January, 2026.

- Importers must calculate, report, and pay for embedded emissions, working closely with suppliers to gather data aligned with EU standards.

- Coolset simplifies CBAM readiness with tools for supplier engagement, emissions tracking, and cost forecasting, all in one platform.

The EU's Carbon Border Adjustment Mechanism (CBAM) is a policy that puts a carbon price on imported goods like steel, aluminium and cement. Now, as of 1 January, 2026, EU-based importers will need to report and pay for the emissions embedded in those goods.

For mid-market enterprises trying to keep up with EU climate regulations, CBAM can feel unnecessarily complex. While proposals to simplify the system are under discussion as part of the EU’s Omnibus package, nothing has been finalized yet.

In the meantime, importers should assume they’re in scope and start preparing now. That means having systems in place to calculate emissions accurately, track supplier data, and prepare for the financial impact of certificate purchases. Failure to comply with CBAM will mean financial penalties, enforcement action, and potential import restrictions.

This guide explains how CBAM works, who it applies to and how your business can prepare.

What is the EU’s Carbon Border Adjustment Mechanism (CBAM)?

CBAM is the EU’s way of pricing the carbon embedded in certain imports. It applies to goods like steel, cement, aluminium, fertilisers, electricity, and hydrogen, all of which are emissions-heavy to produce.

While it’s often called the EU’s “carbon border tax,” or the “import carbon tax” for simplicity, it’s not a tax in the traditional sense. Instead, it’s a mechanism that requires importers to pay for the greenhouse gas (GHG) emissions embedded in specific goods so that they’re treated the same as products made within the EU under its carbon pricing system.

A mechanism to plug “carbon leakage”

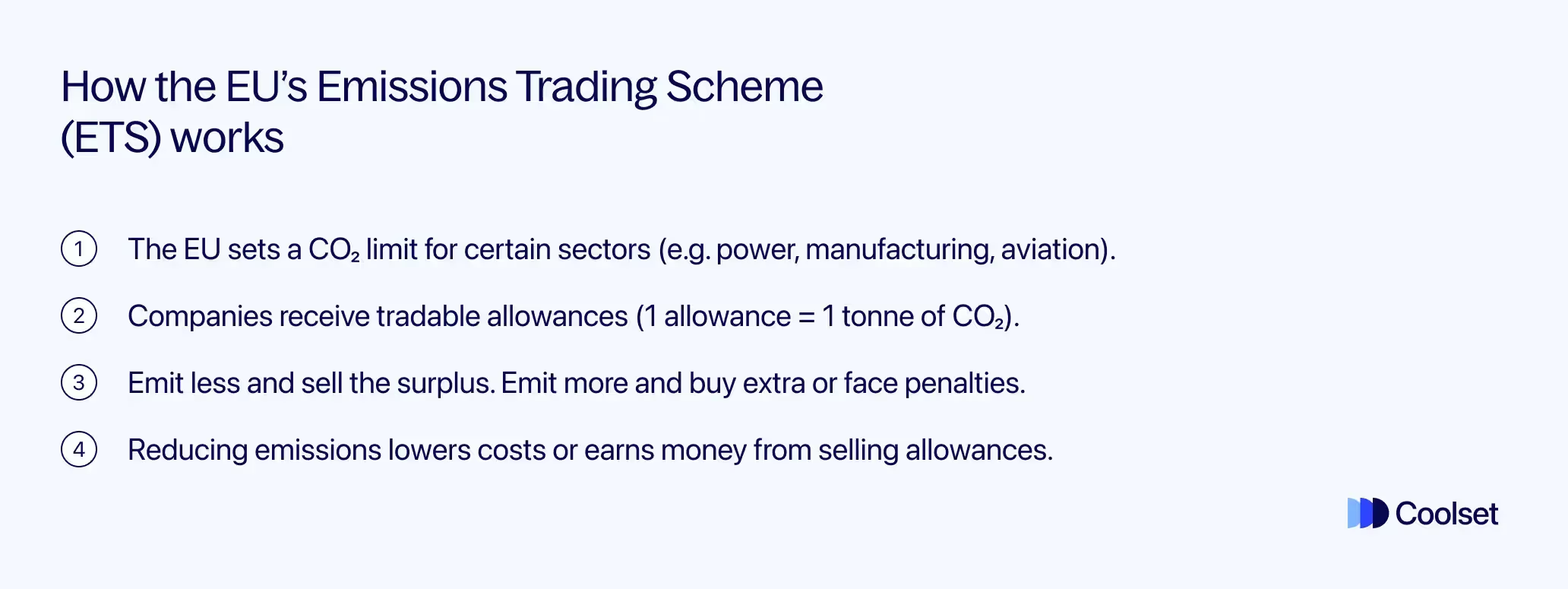

The EU’s Emissions Trading Scheme (ETS) is the bloc’s main tool for cutting industrial emissions.

As of 2023, the ETS has helped bring down emissions in sectors like power and industry plants by around 47% (compared to 2005 levels).

But it has a major limitation: it only applies to production inside the EU.

That means EU-made goods carry a carbon cost, while imported products, often made under weaker environmental rules, do not. This creates a risk of carbon leakage: when companies shift production to countries with looser climate policies, or when high-emission goods are simply imported instead of made in the EU.

CBAM was introduced to close this gap, by placing a comparable carbon price on certain imports. And it makes sense why…

Europe is the world’s largest importer of embedded carbon emissions

The EU imports a significant amount of carbon through goods produced abroad. According to European Parliament data from 2020, more than 20% of the EU’s total CO₂ emissions come from the production of goods and services outside its borders that are consumed within the EU.

That’s roughly 700 million tonnes of CO₂ linked to imports, making the EU the world’s largest importer of what’s known as embedded or virtual carbon.

Without a carbon price on imports, the EU’s efforts to cut emissions at home would be undermined by growing emissions tied to trade.

CBAM levels the playing field

CBAM is the EU’s mechanism to address the emissions embedded in imports. Formally adopted on 17 August 2023, it extends carbon pricing to covered imports through a phased rollout.

Since October 2023, importers have been required to report emissions data. From 1 January 2026, they’ll also need to buy CBAM certificates to cover those emissions, bringing the cost of imports in line with what EU producers already pay under the ETS.

It’s designed so that foreign producers don’t get an unfair advantage, and EU companies aren’t penalized for going greener.

Why is CBAM being implemented by the EU?

As we’ve learnt, CBAM was introduced to close a major gap in EU climate policy: emissions from imported goods. It’s designed to prevent carbon leakage, protect EU industry, and extend the bloc’s decarbonization effort beyond its borders.

Supporting the EU’s ambitious climate targets

CBAM is part of the European Green Deal, the EU’s roadmap to becoming the first climate neutral continent by 2050. It also plays a key role in the Fit for 55 package, which is a set of laws aimed at cutting GHG emissions by 55% by 2030 (compared to 1990 levels).

It complements other EU policies already in motion like the EU Taxonomy for sustainable finance, and the Corporate Sustainability Reporting Directive (CSRD). These policies are aimed at reducing emissions within the EU. CBAM extends that effort to imports, so progress at home isn’t undermined by rising emissions abroad.

CBAM also ties directly into ETS reform. As free emissions allowances for EU producers are phased out from 2026 to 2034, CBAM ensures that imported goods face a comparable carbon cost. The mechanism is designed to be WTO-compliant, applying the same carbon rules to domestic and foreign products based on their emissions.

Driving global decarbonization through trade

As the EU raises its own climate ambition, CBAM puts pressure on trading partners to do the same.

Exporters that want access to the EU market will face a choice: lower the carbon footprint of their products, or pay for the emissions. In this way, CBAM uses the EU’s economic weight to encourage other countries to adopt carbon pricing and cleaner production methods.

How CBAM works: calculate, report, pay

CBAM targets the embedded GHG emissions in certain imported goods. These are the total emissions, mostly CO₂ and in some cases nitrous oxide or PFCs, released during the production of a product, including both:

- Direct emissions from the production process

- Indirect emissions from electricity used in production (only required for some products like cement and fertilisers)

For example, if you import 1 tonne of steel into the EU, you’ll need to account for all the CO₂ emitted by the steel mill abroad to produce that tonne. CBAM ensures a carbon price is paid on those emissions, equivalent to what a European producer would pay under the EU ETS.

{{custom-cta}}

In practice, CBAM will require importers to follow a three-step process for in-scope goods:

1. Calculate emissions

Importers must work out the total direct CO₂ emissions embedded in the goods they bring into the EU. For some products, like cement and fertilisers, certain indirect emissions (like electricity use) also count.

This data needs to come from the non-EU producer, using the EU’s official calculation method, which aligns with the EU ETS.

As of 1 January 2025, importers are required to use only the EU method for calculating emissions. Simplified options, such as default values and equivalent third-country systems, are no longer permitted from this date.

2. Report emissions

From 2026 onward, reporting shifts from a quarterly to an annual format. Importers must submit one verified report each year, and the deadline to do so is end of September. This report forms the basis for surrendering CBAM certificates for the previous calendar year's imports.

Read our CBAM certificate guide to learn how they work, how they’re priced, and what your company needs to do now.

3. Pay via CBAM certificates

From 1 January 2026, importers must buy CBAM certificates to account for the emissions in their goods. Read our outline of what is a CBAM certificate and how do you obtain one.

The price of these certificates will match the average auction price of EU ETS allowances, so EU and non-EU producers are treated equally when it comes to the cost of carbon.

The rules for calculating and reporting emissions vary slightly by sector. The European Commission (EC) has published specific guidance for goods like cement, iron and steel, aluminum, fertilisers, hydrogen, and electricity.

Who needs to comply with CBAM?

CBAM compliance applies to any EU-based importer bringing in covered goods. If you import in-scope products into the EU, whether for your own use or to resell, you’ll need to:

- Register as an authorised CBAM declarant

- Report emissions data

- Purchase CBAM certificates from 2026 onward

If you're a manufacturer or wholesaler based in the EU, you are responsible for CBAM on any imports you bring in.

The EC opened the CBAM declarant registry on 31 March 2025 to allow companies to start the authorization process early. Guidance is available in the “Authorization Management Module” section of the CBAM website.

What about non-EU producers?

Non-EU exporters and producers of the covered goods are indirectly impacted too. While the legal obligation to comply (and pay) lies with the EU importer, foreign producers will need to:

- Provide verified emissions data for their goods

- Potentially lower their products’ carbon footprint to stay competitive (lower emissions = lower CBAM costs)

In practice, CBAM pushes transparency down the supply chain. Importers will need to work closely with their suppliers to get emissions data and encourage improvements.

Countries where CBAM applies

CBAM covers imports from almost all non-EU countries, unless the country participates in the EU ETS or has an equivalent carbon pricing scheme.

Countries exempt from CBAM include:

- Norway, Iceland, and Liechtenstein (all part of the EEA and EU ETS)

- Switzerland (linked to the EU ETS through its own carbon market)

Imports from these countries won’t face CBAM costs. For all other countries, CBAM applies, but any carbon price paid in the country of origin can be deducted, as long as it meets EU criteria.

What products are covered under CBAM?

CBAM currently applies to a targeted list of carbon-intensive goods considered most at risk of carbon leakage.

The initial list includes:

- Iron and steel

- Cement

- Aluminum

- Fertilisers

- Electricity

- Hydrogen

- Plus some precursor and downstream products related to these categories

These sectors were chosen because their production is highly emissions-intensive, and because they’ve historically received free CO₂ allowances under the EU ETS, which are now being phased out.

Each product category maps to specific Combined Nomenclature (CN) codes, listed in Annex I of the CBAM regulation.

Are there any exemptions?

CBAM includes a limited set of exemptions aimed at reducing administrative burden for specific trade flows.

- Low-value consignments: Imports with an intrinsic value below €150 are exempt from CBAM requirements.

- Returned goods: Goods re-imported into the EU without modification are excluded.

- Outward processing: Goods returned to the EU under the outward processing customs procedure are not covered.

- De minimis threshold: A 50-tonne per year de minimis threshold applies to imports of iron and steel, aluminum, cement and fertilizers. Importers below the threshold are exempt from CBAM obligations for those products. Electricity and hydrogen do not use this mass-based threshold.

What are the CBAM reporting requirements?

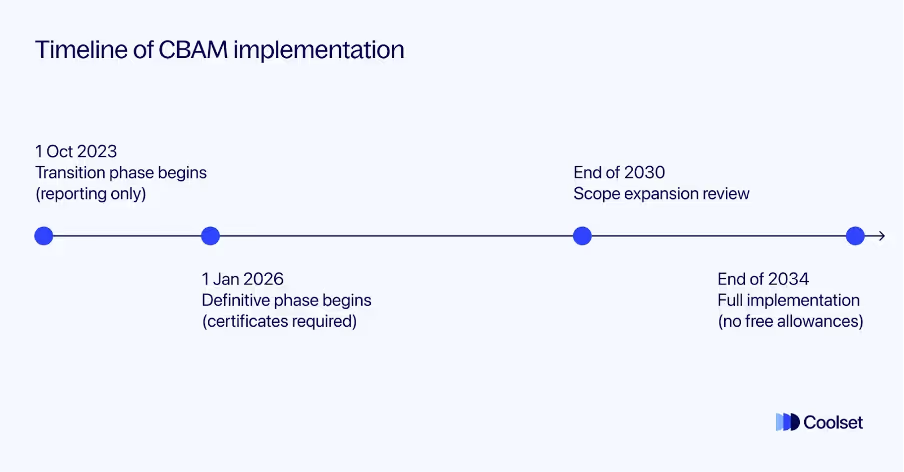

CBAM was rolled out in two main phases: a transitional phase focused on reporting, followed by a definitive phase with full financial enforcement.

Transitional phase (1 Oct 2023 – 31 Dec 2025)

During this phase, importers of CBAM-listed goods were required to submit quarterly reports covering:

- The type and quantity of goods imported

- The country of origin and production site

- Embedded emissions (direct, and indirect where required)

- Any carbon price already paid at origin

Importantly: Importers were not required to pay for emissions. Verification by a third party was also not mandatory.

Definitive phase (from 1 January 2026 onwards)

From 1 January 2026, CBAM moves from a reporting exercise into full enforcement with a carbon pricing obligation. This means importers will need to:

- Register as authorized CBAM declarants

- Buy and surrender CBAM certificates each year, based on the emissions embedded in their imports

- Submit a third-party-verified annual report, due by 30 September each year.

See our detailed article breakdown of the CBAM timeline and phases.

What are CBAM certificates?

CBAM certificates are the EU’s tool for pricing the carbon emissions embedded in certain imported goods. Each certificate represents one tonne of CO₂. The price is based on the weekly average of EU ETS allowance prices, so it reflects the carbon cost faced by EU producers.

When do they become mandatory?

Starting 1 January 2026, importers will need to buy and surrender certificates each year to cover the emissions tied to their in-scope imports. The certificates will become available for purchase from February 2027, covering the entire period from January 2026.

How to obtain and surrender CBAM certificates

Importers will acquire CBAM certificates through a central platform managed by the EC. Only authorized CBAM declarants can access this platform. By 30 September each year, they’ll need to submit a verified CBAM declaration and surrender the corresponding number of CBAM certificates through the CBAM registry.

If fewer are surrendered than required, the shortfall must be made up, and penalties may apply.

What about enforcement and penalties?

Now, failure to surrender enough CBAM certificates will lead to a penalty of €100 per excess tonne. Only authorized declarants will be allowed to import CBAM goods. Unauthorized imports may face even steeper penalties and restrictions.

CBAM timeline and enforcement phases

The CBAM rollout is phased over the coming years, with key milestones for reporting and compliance. Here’s a snapshot of the key dates to know:

1 Oct 2023 – 31 Dec 2025: Transitional phase

- What was required: Importers must submit quarterly reports on the type and quantity of imported goods, embedded emissions, country of origin, and any carbon price already paid abroad.

- No certificates or payments required yet.

- Goal of the phase: To help companies build internal systems, test the reporting process, and prepare for financial enforcement in 2026.

- By Jan 2025: Only the EU's official emissions calculation method is allowed—default values and third-country equivalents are no longer accepted.

- Final quarterly report due: January 2026 (covering Q4 2025)

At the end of 2025: Formal review

The EC is now conducting a formal review of CBAM to assess how the mechanism is functioning so far. The review will also explore whether to expand the scope to include additional product categories, such as organic chemicals and polymers, and whether more indirect emissions, like those from electricity use in manufacturing, should be brought into scope.

1 January 2026 - onward: Definitive phase

- Importers must now:

- Be registered as authorised CBAM declarants

- Submit an annual verified report (due 30 September each year)

- Purchase and surrender CBAM certificates to cover emissions

- Certificate price: Mirrors the weekly average price of EU ETS allowances (€/tonne of CO₂)

- Deductions: If a valid carbon price was paid abroad, that amount can be subtracted from what’s owed.

2026–2030: Gradual expansion and ramp-up

- Financial obligations increase yearly as free EU allowances phase out.

- Scope may expand to cover more products like chemicals, polymers, or glass by 2027–28.

- By 2030, CBAM could apply to all EU ETS sectors, including some indirect emissions.

By 31 December 2034: Full Implementation

- Full phase-out of free ETS allowances for EU producers

- EU producers pay for all their emissions, and importers will be required to do the same via CBAM certificates.

- CBAM fully aligned with EU climate targets.

For a more detailed breakdown of how CBAM will unfold over time, including key compliance deadlines and what to expect from 2025 onwards, read our guide on the CBAM timeline, deadlines, and phases here.

Preparing for a new carbon reality

CBAM marks a shift in how the EU handles carbon in global trade. For sustainability and compliance managers, it introduces a new layer of responsibility: tracking the emissions tied to your imports, reporting them accurately, and paying for them through CBAM certificates.

It’s the EU’s response to carbon leakage, ensuring that as European companies pay for their emissions, foreign producers aren’t given a free pass.

But CBAM compliance isn’t a siloed task. It requires coordination across teams. Procurement will need to gather emissions data from suppliers, sustainability teams will need to calculate product footprints, and finance teams will need to prepare for future certificate costs. Learn how CBAM certificate costs are calculated using real-world examples in our latest article for importers.

If you're a mid-market enterprise, the key is to start now:

- Check whether your imports fall under CBAM

- Register as a declarant

- Begin filing quarterly reports

- And most importantly, start working with your suppliers on emissions data. Many won’t be ready to provide what’s needed.

Also, stay informed. CBAM rules continue to evolve through targeted simplifications. For example, the Omnibus amendments adopted in 2025 introduced a 50-tonne per year de minimis threshold for certain CBAM goods, reducing administrative burden for smaller importers.

At the same time, companies should pay attention to alignment across reporting frameworks. While CBAM disclosures are separate from European Sustainability Reporting Standards (ESRS), using consistent emissions data and methodologies can reduce duplication and improve audit readiness. Learn how recent ESRS simplifications affect emissions-related reporting in our June 2025 ESRS update.

CBAM may evolve, but the direction is clear: carbon accountability is becoming part of the cost of doing business. And those who prepare early will be better positioned, both for compliance and competitiveness.

{{cbam-calculator-injectable}}

Need help getting CBAM-ready?

Coolset helps companies streamline sustainability and ESG reporting, so you're not just reacting to regulations, but building the systems to stay ahead. Get in touch to find out how we can help you get ready for CBAM compliance.

How to translate CBAM reporting inputs into predictable, auditable cost exposure now

on mobile screens

to experience this demo.

↘ Check if your documentation meets PPWR requirements

This free compliance checker scans your packaging documentation and maps it against mandatory PPWR data requirements, giving you a clear view of your compliance status. Get actionable insights on documentation gaps before they become compliance issues.

From zero to CBAM compliant in a few weeks

Get the tools, structure and support you need to meet CBAM requirements with no prior experience or systems.

.webp)