Disclaimer: New EUDR developments - December 2025

In November 2025, the European Parliament and Council backed key changes to the EU Deforestation Regulation (EUDR), including a 12‑month enforcement delay and simplified obligations based on company size and supply chain role.

Key changes proposed:

- New enforcement timeline: 30 December 2026 for large/medium operators, 30 June 2027 for small/micro operators

- Simplified DDS: One-time declarations for small and micro primary producers

- Narrowed scope: Most downstream actors and non‑SME traders would no longer need to submit DDSs

- New DDS requirement: Estimated annual quantity of regulated products must be included

These updates are not yet legally binding. A final text will be confirmed through trilogue negotiations and formal publication in the EU’s Official Journal. Until then, the current EUDR regulation and deadlines remain in force.

We continue to monitor developments and will update all guidance as the final law is adopted.

Disclaimer: 2026 Omnibus changes to CSRD and ESRS

In December 2025, the European Parliament approved the Omnibus I package, introducing changes to CSRD scope, timelines and related reporting requirements.

As a result, parts of this article may no longer fully reflect the latest regulatory position. We are currently reviewing and updating our CSRD and ESRS content to align with the new rules.

Key changes include:

- A narrowed CSRD scope, now limited to companies with 1,000+ employees and €450m turnover

- Delays to CSRD reporting timelines, with wave 2 and 3 reports pushed to 2028/2029 in most cases

- Simplification of ESRS datapoints

We continue to monitor regulatory developments closely and will update this article as further guidance and implementation details are confirmed.

{{updated}}

Die Einhaltung der Corporate Sustainability Reporting Directive (CSRD) erfordert mehr als nur das Sammeln von Daten. Es geht darum, sicherzustellen, dass Ihre Nachhaltigkeitsinformationen sowohl glaubwürdig als auch bedeutungsvoll für die Nutzer sind.

Um dies zu erleichtern, definiert die CSRD fünf wesentliche qualitative Merkmale, an die sich Ihre Offenlegungen halten müssen: Relevanz, getreue Darstellung, Vergleichbarkeit, Überprüfbarkeit und Verständlichkeit. Diese Standards stellen sicher, dass Ihre Nachhaltigkeitsdaten prüfsicher, zuverlässig und wertvoll für alle Beteiligten sind.

Das Nichterfüllen dieser Standards kann zu kostspieligen Verzögerungen und Nacharbeiten führen. Indem Sie Ihre Berichterstattung von Anfang an an diesen Merkmalen ausrichten, können Sie zeitaufwändige Überarbeitungen vermeiden und die Compliance-Kosten niedrig halten.

Dieser Artikel fasst die Kernelemente der CSRD zusammen und erklärt die fünf qualitativen Merkmale, die Ihre Nachhaltigkeitsdaten erfüllen müssen.

CSRD, ESRS, doppelte Wesentlichkeitsbewertungen: Wie hängen sie zusammen?

,Bevor wir uns den fünf qualitativen Merkmalen zuwenden, fassen wir kurz einige Schlüsselelemente der CSRD zusammen.

Die Corporate Sustainability Reporting Directive (CSRD)

Die CSRD ist der aktualisierte Rahmen der EU zur Verbesserung der Transparenz und Rechenschaftspflicht in der Unternehmensnachhaltigkeitsberichterstattung. Sie ersetzt und erweitert die vorherige Richtlinie zur nichtfinanziellen Berichterstattung (NFRD) und bietet Investoren und Verbrauchern eine klarere Möglichkeit, die Auswirkungen von Unternehmen auf Umwelt, Soziales und Unternehmensführung (ESG) zu bewerten und zu vergleichen.

Eingeführt im Rahmen des Europäischen Green Deals, unterstützt die CSRD das Ziel der EU, bis 2050 der erste klimaneutrale Kontinent zu werden und die globale Erwärmung gemäß dem Pariser Abkommen unter 1,5°C zu halten.

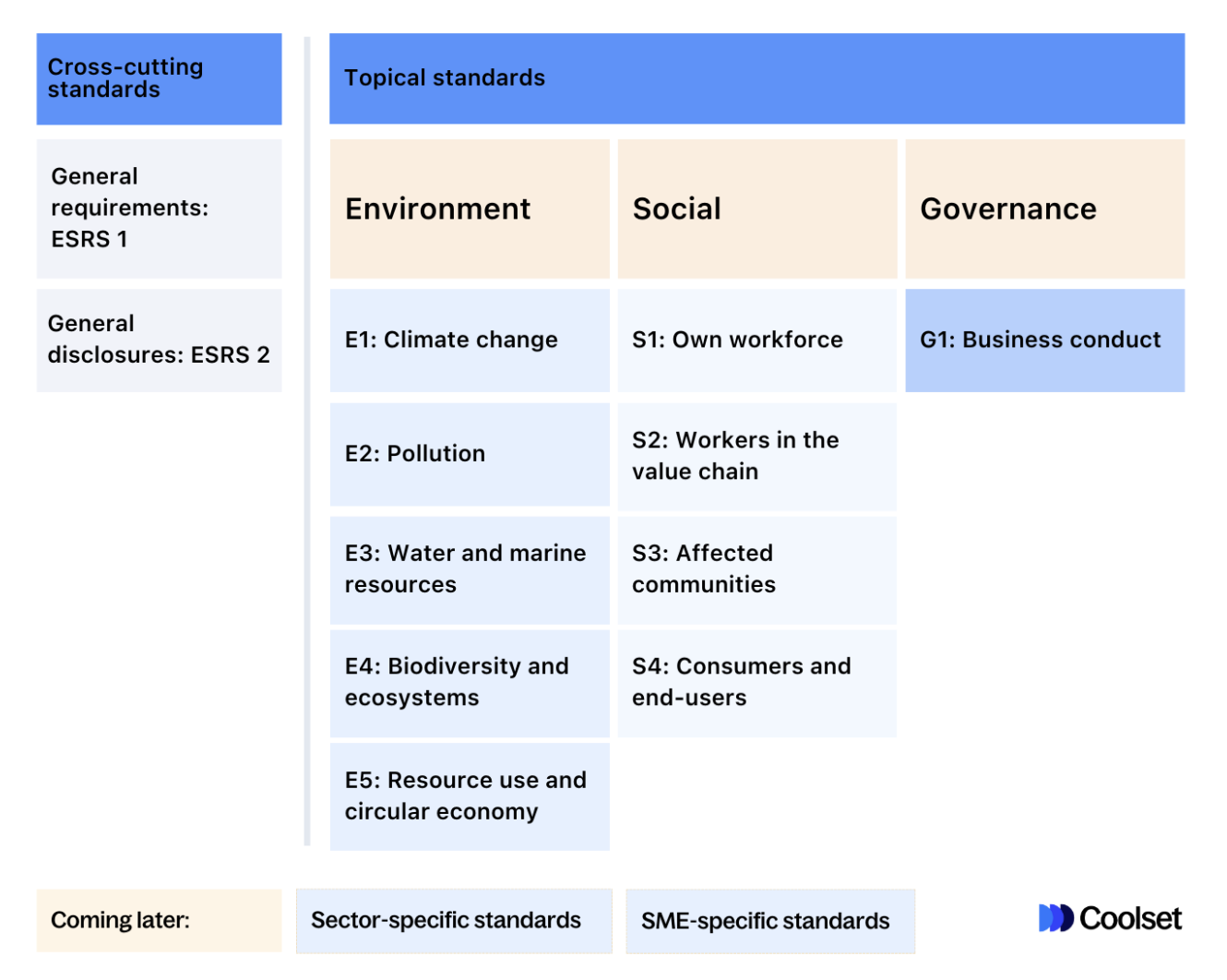

Die europäischen Nachhaltigkeitsberichtsstandards (ESRS)

Die ESRS bilden den Rahmen der CSRD. Diese Standards legen die spezifischen Berichtsanforderungen für Unternehmen fest, um sicherzustellen, dass Nachhaltigkeitsberichte vergleichbar, genau und aussagekräftig sind.

Es gibt insgesamt 12 Standards, von denen 10 sich auf spezifische ESG-Themen konzentrieren. Die verbleibenden zwei übergreifenden Standards bieten allgemeine Offenlegungsleitlinien, die für alle Unternehmen gelten.

Bis zum 30. Juni 2026 werden sektorspezifische Standards und Offenlegungen für Nicht-EU-Unternehmen eingeführt, um die Berichtsanforderungen weiter auf verschiedene Branchen zuzuschneiden. Beachten Sie, dass der Omnibus-Vorschlag darauf abzielt, diese sektorspezifischen Standards abzuschaffen.

Die doppelte Wesentlichkeitsbewertung

Die doppelte Wesentlichkeitsbewertung ist der obligatorische erste Schritt zur Einhaltung der CSRD. Sie hilft Ihnen zu bestimmen, welche der 10 thematischen Standards in Ihre Berichte aufgenommen werden sollten.

Themen können aufgrund ihrer Auswirkungen auf die finanzielle Leistung Ihres Unternehmens (finanzielle Wesentlichkeit), ihrer Wirkung auf Gesellschaft und Umwelt (Auswirkungswesentlichkeit) oder beidem wesentlich sein.

Durch die Bewertung Ihres Unternehmens durch diese beiden Linsen stellen Sie sicher, dass die offengelegten Informationen das widerspiegeln, was sowohl für Ihr Unternehmen als auch für seine Stakeholder wirklich wichtig ist.

{{custom-cta}}

Datenqualitätsanforderungen: 5 qualitative Merkmale der CSRD-Berichterstattung

Nachdem Sie Ihre wesentlichen Themen identifiziert haben, besteht der nächste Schritt darin, die erforderlichen Daten zu sammeln und Ihren Bericht vorzubereiten. Die Offenlegungsqualitäten der CSRD während des gesamten Compliance-Prozesses im Fokus zu behalten – einschließlich der doppelten Wesentlichkeitsbewertung – stellt sicher, dass Ihre Berichte zuverlässig und prüfungssicher sind.

Werfen wir nun einen genaueren Blick auf die fünf qualitativen Merkmale:

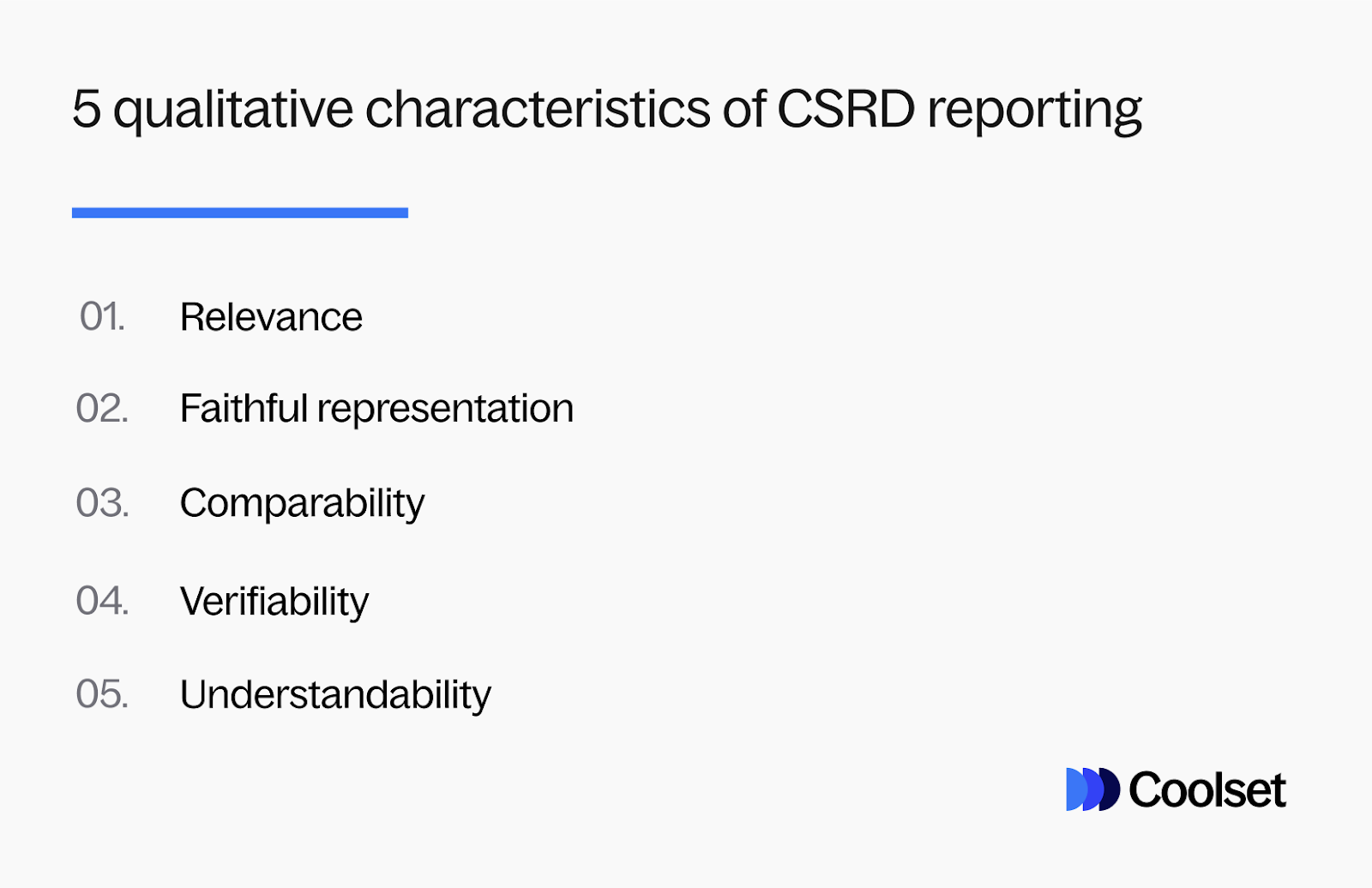

1. Relevanz

Das erste qualitative Merkmal von CSRD-Daten ist die Relevanz. Relevante Informationen sollten die Fähigkeit haben, Bewertungen und Entscheidungen zu beeinflussen, sei es, um Stakeholdern zu helfen, zukünftige Ergebnisse vorherzusagen oder vergangene Bewertungen zu bestätigen oder zu ändern.

Das bedeutet, dass Ihre Daten offen, transparent und klar über Nachhaltigkeitsthemen kommunizieren sollten, wobei der Kontext und die Bedeutung der bereitgestellten Informationen berücksichtigt werden.

2. Getreue Darstellung

Getreue Darstellung bedeutet, Dinge so zu zeigen, wie sie wirklich sind. Informationen bieten eine getreue Darstellung der Realität, wenn sie vollständig, neutral und genau sind.

- Eine vollständige Offenlegung deckt alle wesentlichen Informationen zum Thema ab, mit angemessenen Beschreibungen und Erklärungen, die den Nutzern das geben, was sie für fundierte Entscheidungen benötigen.

- Neutralität bedeutet, die Fakten ohne Voreingenommenheit darzustellen und eine ausgewogene Sicht auf Risiken, Chancen und Auswirkungen zu bieten – ohne einen einseitigen Fokus auf positive oder negative Aspekte.

- Genauigkeit bedeutet, dass Ihre Daten klar sein sollten, ohne Verrechnung oder Kompensation von Zahlen, und Schätzungen und deren Einschränkungen klar hervorheben. Während Genauigkeit nicht perfekt sein muss, sollten die Informationen so nah wie möglich an der Realität sein.

Die Eigenschaften Vergleichbarkeit, Überprüfbarkeit und Verständlichkeit tragen ebenfalls dazu bei, die Daten nützlicher zu machen.

3. Vergleichbarkeit

Vergleichbarkeit erhöht die Nützlichkeit Ihrer Informationen, indem sie sicherstellt, dass sie über die Zeit hinweg konsistent sind und leicht über und innerhalb von Sektoren verglichen werden können. Ihre Daten sollten mit einem Referenzpunkt wie einem Basiswert, Ziel oder Branchenmaßstab übereinstimmen und Jahr für Jahr konsistente Berichterstattungsmethoden verwenden.

In der Nachhaltigkeitsberichterstattung sollten sowohl Rohdaten als auch normalisierte Daten priorisiert werden, da sie klare und faire Vergleiche bieten. Relative Daten wie Prozentsätze haben immer noch Wert, auch wenn sie allein nicht so umfassend sind.

4. Überprüfbarkeit

Nachhaltigkeitsinformationen sind überprüfbar, wenn sie es den Nutzern ermöglichen, den Daten zu vertrauen, die ihre Entscheidungen informieren, und es verschiedenen unabhängigen Beobachtern mit angemessener Expertise ermöglichen, zu ähnlichen Schlussfolgerungen zu gelangen. Überprüfbare Informationen sollten nachvollziehbar und prüfbar sein, mit klarer Dokumentation der Prozesse und Methoden, die zur Erstellung der Informationen verwendet wurden.

5. Verständlichkeit

Verständliche Informationen werden klar und prägnant präsentiert, sodass die Nutzer die Hauptpunkte erfassen können. Sie sollten in leicht nachvollziehbaren Formaten wie Tabellen, Grafiken und Diagrammen neben erzählendem Text dargestellt werden, um wichtige Aspekte hervorzuheben.

Selbst komplexe Informationen sollten so klar wie möglich präsentiert werden. Vermeiden Sie unnötigen Fachjargon und Abkürzungen und fügen Sie Maßeinheiten hinzu, um die Informationen zugänglich zu halten.

.webp)

Beschleunigen Sie Ihre CSRD-Compliance-Reise mit der richtigen Software

Wie Sie sehen, umfasst die Einhaltung der CSRD weit mehr als nur das Sammeln von Daten – es geht darum, sicherzustellen, dass Ihre Nachhaltigkeitsinformationen zuverlässig und für alle beteiligten Stakeholder nützlich sind. Indem Sie die fünf Qualitätsstandards von Anfang an im Auge behalten, können Sie kostspielige Verzögerungen vermeiden und sicherstellen, dass Ihre Offenlegungen den Erwartungen der Stakeholder entsprechen.

Um diesen Prozess effizienter zu gestalten, automatisiert die Nachhaltigkeitsmanagement-Software von Coolset jeden Schritt Ihrer CSRD-Compliance-Reise.

Vorgefertigte Umfragen führen Sie durch die doppelte Wesentlichkeitsbewertung, wobei die Ergebnisse auf einer Wesentlichkeitsmatrix visualisiert werden. Basierend auf diesen Ergebnissen schaltet die Software nur die relevanten ESRS-Offenlegungen frei, sodass Sie keine Zeit mit der Datenerfassung verschwenden, die Sie nicht benötigen.

Mit kuratierten Antwortvorschlägen und der Möglichkeit, unterstützende Nachweise anzuhängen, können Sie Ihren Bericht schnell abschließen und im erforderlichen .XBRL-Format exportieren, bereit für die Prüfung.

Bereit, loszulegen? Probieren Sie Coolset selbst aus oder fordern Sie noch heute eine kostenlose, personalisierte Einführung von einem unserer Produktexperten an.

{{product-tour-injectable}}

Written by our in-house sustainability experts

auf mobilen Bildschirmen

um diese Demo zu erleben.

Know your EUDR obligations

Answer a few quick questions to identify your role in the EUDR supply chain, your compliance deadline, and the exact steps you need to take. No e-mail required.