ESRS E1 climate reporting: what changes under the amended ESRS (2026)

Disclaimer: New EUDR developments - December 2025

In November 2025, the European Parliament and Council backed key changes to the EU Deforestation Regulation (EUDR), including a 12‑month enforcement delay and simplified obligations based on company size and supply chain role.

Key changes proposed:

- New enforcement timeline: 30 December 2026 for large/medium operators, 30 June 2027 for small/micro operators

- Simplified DDS: One-time declarations for small and micro primary producers

- Narrowed scope: Most downstream actors and non‑SME traders would no longer need to submit DDSs

- New DDS requirement: Estimated annual quantity of regulated products must be included

These updates are not yet legally binding. A final text will be confirmed through trilogue negotiations and formal publication in the EU’s Official Journal. Until then, the current EUDR regulation and deadlines remain in force.

We continue to monitor developments and will update all guidance as the final law is adopted.

Key Takeaways

- The Amended ESRS E1 expands climate reporting from 9 to 11 disclosure requirements under CSRD, with the finalized standards expected to apply from January 1, 2027.

- EFRAG submitted the amended standards to the European Commission in November 2025; adoption as a delegated act is expected by mid-2026.

- Companies concluding climate change is not material must now explicitly justify that conclusion.

- Coolset helps companies collect emissions data, structure ESRS E1 disclosures, and generate CSRD-compliant reports automatically.

The Corporate Sustainability Reporting Directive (CSRD) has already transformed how companies report sustainability performance, but the regulatory landscape is still evolving. At the end of November 2025, EFRAG submitted the Amended European Sustainability Reporting Standards (ESRS) to the European Commission as technical advice following the Omnibus Proposal.

The Amended ESRS E1 is more proportional and clearer about what matters in climate reporting. It cuts unnecessary datapoints, refocuses expectations around transition planning, climate risk analysis, and emissions data, and gives companies more flexibility where value chain data is hard to obtain. At the same time, it does not lower the bar on substance. If climate change is material, companies still need a credible transition plan, defensible targets, and a clear connection to financial decision-making.

The drafts submitted by EFRAG are now with the European Commission, which is expected to finalise and adopt the amended standards as a delegated act by mid-2026, aiming for them to apply for reporting periods beginning on or after January 1, 2027.

With CSRD scope and timing still in flux, understanding the Amended ESRS E1 and how to apply it in practice remains essential. This guide explains what has changed, why climate disclosures remain central, and what companies should prioritise next.

What is ESRS E1 exactly?

The European Sustainability Reporting Standards (ESRS) were adopted by the European Commission in July 2023 to standardise sustainability reporting under the Corporate Sustainability Reporting Directive (CSRD). They define how companies must structure their CSRD reports and what to disclose across environmental, social, and governance topics.

The first set of ESRS includes 10 topical standards and two cross-cutting standards. ESRS E1 is the climate change standard. It requires companies to disclose material information across three climate-related sub-topics:

- climate change mitigation

- climate change adaptation

- energy

In practical terms, ESRS E1 focuses on how climate change affects the business and how the business affects the climate. The standard requires transparency on:

- climate strategy, including transition planning and the identification of climate-related risks

- the resilience of the business model and strategy under climate-related scenarios

- policies, actions, and resources used to manage climate impacts, risks, and opportunities

- metrics and targets, including energy use, greenhouse gas emissions, carbon removals and credits, and internal carbon pricing

- anticipated financial effects from material physical and transition risks, as well as material climate-related opportunities

Together, these disclosures are designed to show whether a company understands its climate exposure, has a credible plan to reduce emissions, and is prepared for a low-carbon transition.

The total set of ESRS's comprise of 10 primary topics and two cross-cutting standards. As you can see in the below table, E1: Climate change is the first of five environmental standards.

As the name suggests, ESRS E1 requires organizations to disclose their impacts on climate change. This includes the positive and negative consequences of their business activities – from energy consumption to sourcing materials across value chains.

It also demands transparency around actual and potential impacts as well as past, present, and future efforts to tackle climate change.

The importance of ESRS E1 for climate change

The CSRD was introduced as part of the European Green Deal: a framework to transition Europe to the first climate-neutral continent by 2050, and to keep global warming to 1.5°C in line with the Paris Agreement.

This ambitious goal reflects the urgency of the current climate crisis, with the earth warming at a rate not seen in the past 10,000 years.

In this context, it’s clear that the climate change component is a top priority for Europe. That’s why ESRS E1 stands out as the most detailed reporting standard. Its ultimate goal is to ensure business practices align with Europe’s ambitious climate objectives.

While more and more countries are committing to net zero emissions by 2050, research shows that half of the necessary emissions must be cut by 2030 to keep warming below 1.5°C.

This makes compliance with ESRS E1 not just a regulatory obligation but a crucial part of global efforts to effectively manage and mitigate climate change.

What changed in climate change materiality under the Amended ESRS E1

Under the original ESRS, companies could conclude that climate change was not material, but expectations around how to justify that conclusion were less explicit. The Amended ESRS E1 tightens this logic.

If a company now concludes that climate change is not material and therefore omits all disclosures under ESRS E1, it must clearly disclose the basis for that conclusion. This turns “non-material climate” into a position that needs to be actively justified, rather than passively assumed.

The amended standard also clarifies the structure of ESRS E1. Climate change is explicitly split into three sub-topics: climate change mitigation, climate change adaptation, and energy. Companies can assess materiality at sub-topic level and apply the standard ESRS materiality rules accordingly.

In practice, this leaves little room for omission. EFRAG’s 2025 State of Play report shows that 98% of 646 companies analysed mapped ESRS E1 as material, confirming that climate change is material for almost all reporting entities in scope.

Climate change reporting within the CSRD framework

The CSRD allows companies to omit reporting on certain themes if they are not material – but ESRS E1 holds a special requirement.

Unlike other ESRS standards, if a company deems ESRS E1 as non-material, it must provide detailed justification as well as a forward-looking analysis on what could make the topic material in the future.

In practice, this makes it extremely challenging for companies to exclude this standard given the near-universal impact of GHG emissions across business activities.

And it shouldn’t be avoided anyway.

Consumers, employees, investors, and governments are demanding more transparency around corporate sustainability. Failing to report under ESRS E1 could negatively impact your company’s reputation and stakeholder trust.

{{custom-cta}}

The 11 ESRS E1 disclosure requirements (updated)

The Amended ESRS E1 expands the standard from 9 to 11 disclosure requirements and restructures several topics. The most notable change is the clearer separation of climate risk identification and scenario analysis and climate resilience into standalone disclosures. Let’s take a look at its highly structured requirements in more detail:

Strategy

E1-1 Transition plan for climate change mitigation

Companies must disclose whether they have a transition plan for climate change mitigation and how it aligns the business model and strategy with limiting global warming to 1.5°C and achieving climate neutrality by 2050, in line with EU climate objectives.

At a minimum, companies must disclose:

- Whether a transition plan exists: If no plan is in place, this must be stated, along with whether and when the company expects to adopt one.

- A summary of the key elements of the transition plan, including:

- greenhouse gas (GHG) emission reduction targets

- the main decarbonisation levers and mitigation actions

- investments and funding supporting the plan

- whether the plan is approved by the administrative, management, or supervisory bodies

- how the plan is embedded in overall strategy and financial planning

- an explanation of how the plan is compatible with limiting warming to 1.5°C and reaching climate neutrality by 2050

- greenhouse gas (GHG) emission reduction targets

- Capital expenditure linked to fossil fuels: The amount of CapEx invested during the reporting period in coal, oil, and gas activities, where applicable.

- Key assumptions and dependencies: The main assumptions underpinning the transition plan, such as policy developments, technology availability, market uptake, infrastructure, and value chain constraints.

- Locked-in emissions: A qualitative assessment of potential locked-in greenhouse gas emissions from key assets and products.

- Implementation progress: A clear explanation of progress made in implementing the transition plan during the reporting period.

Practical tip: ESRS E1 explicitly allows companies to present key elements of the transition plan, such as targets, decarbonisation levers, and actions, in tables or visuals. Use this flexibility. It significantly improves clarity and readability.

E1-2 Identification of climate-related risks and scenario analysis

This disclosure requirement is one of the most important structural updates in the Amended ESRS E1. It focuses on how companies identify and assess climate-related risks and opportunities from a financial materiality perspective, and how robust that assessment process is.

Companies must disclose:

- Risk classification: For each material climate-related risk, whether it is a physical risk or a transition risk.

- Risk identification and assessment methodology: The key elements of the methodology used to identify and assess exposure and sensitivity of assets and activities across own operations and the value chain. This must cover short-, medium-, and long-term time horizons and consider both climate hazards and transition events or trends.

- Level of methodological detail: In practice, this means being specific about what was screened, which data sources were used, how likelihood and severity were assessed, and how climate hazards or transition events were linked to concrete business impacts.

- Scenario analysis, where applied: If climate-related scenario analysis is used, companies must disclose:

- the range of scenarios applied

- at least one high-emissions scenario for assessing physical risks and at least one 1.5°C no or limited overshoot scenario for assessing transition risks

- the related global temperature projections and why they are relevant

- the scope of operations and value chain covered, key assumptions, and when the analysis was carried out

- the range of scenarios applied

Practical tip: Treat this disclosure as a method description rather than a results summary. Document the process clearly and consistently, so it can be reused across reporting cycles and linked to financial risk management and strategy discussions.

E1-3 Resilience in relation to climate change

This disclosure requirement focuses on what climate risk analysis means for the business strategy and business model in practice.

Companies must disclose:

- Results of the climate resilience analysis, including:

- implications for the strategy and business model

- how climate-related scenario analysis, where used, informs potential strategic responses

- how the transition plan and mitigation or adaptation actions contribute to climate resilience

- implications for the strategy and business model

- Key uncertainties: The most significant uncertainties that affect the resilience assessment.

- Adaptive capacity: The company’s capacity to adjust or adapt its strategy and business model over short-, medium-, and long-term time horizons.

Practical tip: Use this section to synthesise insights rather than repeat technical analysis. Clearly explain which climate risks matter most, how they could affect the business first, which responses are already in place, and where resilience remains limited. This disclosure should build directly on the E1-2 risk analysis and connect to E1-11, where assets and revenue at risk are quantified.

{{product-tour-injectable}}

Impact, Risk, and Opportunity Management

E1-4 Policies related to climate change mitigation and adaptation

This disclosure requirement is streamlined in the Amended ESRS E1.

Companies must disclose their climate-related policies in line with the general policy disclosure requirements set out in ESRS 2. For each material climate-related matter, this means clearly describing the policies in place to manage climate change mitigation and adaptation, including how these policies guide identification, assessment, and management of material impacts, risks, and opportunities.

The focus is on clarity and relevance, not on duplicating policy language across multiple sections of the report.

E1-5 Actions and resources related to climate change mitigation and adaptation

Companies must disclose their key climate change mitigation and adaptation actions, along with the resources allocated to implement them, in line with the action and resource disclosure requirements in ESRS 2.

The Amended ESRS E1 places clearer emphasis on structure and outcomes. When disclosing current and planned actions, companies must:

- present key mitigation actions grouped by decarbonisation lever

- disclose achieved and expected greenhouse gas emission reductions for each lever

This shifts the focus away from unstructured action lists and toward a coherent action portfolio that is directly linked to quantified emissions outcomes.

Practical tip: Start from the emissions inventory and work backwards. Map each major emissions source to one or more decarbonisation levers, then link concrete actions and expected reductions to those levers. This makes the disclosure easier to maintain and much harder to challenge.

Metrics and targets

E1-6 Targets related to climate change

Companies must disclose their climate-related targets in line with the target disclosure requirements set out in ESRS 2.

For greenhouse gas emission reduction targets, companies must disclose:

- Target type and scope: Absolute emission reduction targets for Scope 1, Scope 2, and Scope 3 emissions, disclosed separately or combined. Where relevant, companies may also disclose intensity targets. In all cases, it must be clear which scopes are included and, if combined, the share covered by each scope.

- Consistency with the GHG inventory: If the scope of the targets differs from the scope of the greenhouse gas inventory, companies must explain the divergence and disclose the percentage of emissions and greenhouse gases covered by the targets.

- Science alignment: Whether targets are science-based and compatible with limiting global warming to 1.5°C, including the framework, methodology, and climate scenarios used to set them.

- Key assumptions: A brief explanation of the main assumptions that affect emissions trajectories and target achievement, such as changes in sales volumes, demand, regulation, or technology uptake.

The Amended ESRS E1 also introduces two important clarifications:

- Targets must be gross: Emission reduction targets must not rely on greenhouse gas removals, carbon credits, or avoided emissions.

- Absolute values remain required: When companies disclose intensity targets only, they generally must also disclose the corresponding absolute emission values for the target year and interim years, with limited exceptions for certain financial institutions.

Practical tip: When explaining alignment with 1.5°C, compare targets against a relevant sector-specific or cross-sector 1.5°C pathway and benchmark them against a 1.5°C-aligned reference target. This makes the science alignment clear and defensible.

E1-7 Energy consumption and mix

Companies must disclose total energy consumption from their own operations, expressed in megawatt hours (MWh), disaggregated by:

- fossil energy sources

- nuclear energy sources

- renewable energy sources

Additional disclosure requirements apply in specific cases:

- High climate impact sectors: Companies operating in high climate impact sectors must further disaggregate fossil energy consumption into coal, oil, gas, other fossil fuels, and purchased or acquired electricity, heat, steam, or cooling generated from fossil sources.

- Energy production activities: Companies that produce energy must separately disclose the amount of non-renewable and renewable energy produced, expressed in MWh.

The Amended ESRS E1 also clarifies how energy consumption must be calculated. When preparing this disclosure, companies must:

- exclude feedstocks that are not combusted for energy purposes, such as gas used as a chemical feedstock

- use MWh based on lower heating value for combustion-related information

- base figures on final energy consumption

- avoid double counting self-generated energy

- clearly state whether renewable energy shares are calculated using a market-based or location-based approach, and only count renewable energy under the market-based approach where renewable attributes are clearly defined in contractual instruments such as power purchase agreements or Guarantees of Origin

Practical tip: Align energy accounting early with greenhouse gas accounting. Using consistent boundaries and assumptions across energy and emissions data avoids reconciliation issues later in the CSRD report.

E1-8 Gross Scopes 1, 2, and 3 GHG emissions

Companies must disclose absolute gross greenhouse gas emissions for the reporting period, expressed in tonnes of CO₂ equivalent.

At a minimum, this includes:

Scope 1 emissions: Direct emissions from owned or controlled sources, including the percentage of Scope 1 emissions covered by the EU Emissions Trading System, where applicable.

Scope 2 emissions: Indirect emissions from purchased or acquired electricity, heat, steam, and cooling, disclosed using both location-based and market-based methods.

Scope 3 emissions: Indirect emissions across the value chain, disclosed as a total and broken down by each significant Scope 3 category.

In addition, companies must disclose direct biogenic CO₂ emissions from biomass combustion or biodegradation separately from Scope 1 emissions.

The Amended ESRS E1 also clarifies several key methodological requirements:

- Reporting boundary: Emissions reporting starts from a financial control boundary. If this does not adequately represent emissions from operated assets outside that boundary, companies must also disclose Scope 1 and Scope 2 emissions using an operational control approach.

- Gross emissions only: Emissions totals must exclude greenhouse gas removals, carbon credits, and emissions allowances.

- Treatment of biogenic emissions: Biogenic CO₂ must not be included in Scope 1, Scope 2, or Scope 3 totals. Other greenhouse gases from biomass, such as CH₄ and N₂O, must be included where relevant.

- Scope 3 methodology: Companies must apply a structured approach to Scope 3 emissions by screening all 15 Scope 3 categories, identifying significant categories, updating significant categories annually, and refreshing the full Scope 3 inventory at least every three years or sooner if major changes occur.

Practical tip: Document Scope 3 screening decisions and assumptions in detail. This makes it easier to explain why certain categories are considered significant, defend estimates during assurance, and maintain consistency across reporting cycles.

E1-9 GHG removals and carbon credits

This disclosure requirement focuses on transparency and integrity. Companies must clearly distinguish between greenhouse gas removals within their operations or value chain and carbon credits financed outside the value chain, and explain how these activities relate to emissions reduction targets.

If a company implements GHG removal and storage projects, it must disclose:

- a brief description of each project

- the amount of removals or storage achieved through each project

- how non-permanence risks are managed, including leakage and reversal monitoring

- any reversals that occurred during the reporting period, which must be deducted from reported removals

For carbon credits linked to projects outside the company’s operations and value chain, companies must disclose:

- the amount of credits verified and cancelled during the reporting period

- the amount of credits purchased but not yet cancelled

- the share of credits originating from removal projects, with a clear distinction between nature-based and technological removals

Where companies make public claims related to greenhouse gas neutrality that rely on carbon credits, they must explain how these claims do not undermine their emission reduction targets and how credit quality and integrity are ensured. This includes addressing additionality, permanence, leakage risk, avoidance of double counting, and verifiability.

Practical tip: Keep reduction targets, removals, and carbon credits strictly separated in internal reporting. This reduces the risk of inconsistent claims and makes it easier to defend disclosures to auditors, regulators, and stakeholders.

E1-10 Internal carbon pricing

Where a company uses internal carbon pricing, it must disclose how carbon pricing is applied in decision-making to support emissions reduction objectives. This includes explaining whether and how the carbon price or prices used are consistent with those applied in financial statements, particularly for asset valuation and impairment testing.

Companies must also disclose the average carbon price per tonne applied under each internal carbon pricing scheme during the reporting period.

Practical tip: Align internal carbon prices with the assumptions used in capital allocation and asset valuation. Inconsistencies between sustainability disclosures and financial models are a common red flag during assurance.

E1-11 Anticipated financial effects from material physical and transition risks and climate-related opportunities

This disclosure requirement makes the link between climate change and financial performance explicit. Companies must show which assets and revenues are exposed to climate-related risks and opportunities, and how those exposures are assessed.

For material physical risks, companies must disclose:

- the carrying amount of assets materially exposed to physical climate risks before adaptation measures

- the percentage of those assets covered by adaptation actions

- the net revenue generated from activities exposed to physical climate risks

For material transition risks, companies must disclose:

- the carrying amount of assets exposed to transition risks and a range of estimated potential stranded assets, based on analysis of 1.5°C-aligned scenarios

- the percentage of transition-risk assets addressed by mitigation actions

- where relevant, additional information such as the breakdown of real estate assets used as loan collateral by energy efficiency classes, estimated potential liabilities, and net revenue at transition risk, including exposure to affected customers

For climate-related opportunities, where these are expected to be material, companies must disclose the carrying amount of assets and the net revenue aligned with those opportunities.

In all cases, companies must clearly disclose the methodology and assumptions used, the data sources applied, and the major uncertainties affecting the estimates.

Practical tip: Involve finance teams early. These disclosures rely on asset registers, revenue segmentation, and valuation assumptions that typically sit outside sustainability teams, and late alignment is one of the most common causes of reporting gaps.

Practical steps for implementing ESRS E1 Disclosure Requirements

Implementing the ESRS E1 is a vital part of CSRD compliance. Here are some straightforward steps to help your cross-functional team implement these requirements effectively:

1. Conduct a materiality assessment

Businesses are not required to report on all sub-topics described in the topical ESRS, only on those that are material, i.e. significant to their business.

Performing a double materiality assessment helps you determine which topics are material and which are not. It’s the process of identifying and prioritizing the most significant ESG matters to report on.

It should be based on the principle of ‘double materiality’ meaning considering both impact materiality and financial materiality when identifying the material matters.

When conducting a materiality assessment for ESRS E1, there are three subtopics to consider:

Sub-topic 1: Climate change adaptation

Evaluates how a company identifies risks and opportunities presented by climate change and adjusts its operations, strategies, and investments to mitigate those risks and capitalize on opportunities.

Sub-topic 2: Climate change mitigation

Focuses on the actions a company takes to reduce its greenhouse gas emissions and its carbon footprint, aiming to contribute to the global effort to limit the effects of climate change.

Sub-topic 3: Energy

Assesses a company's energy use, including the efficiency of its energy consumption and the extent to which it incorporates renewable energy sources into its operations, to reduce its environmental impact and improve sustainability.

Unsure where to begin? Download our free double materiality assessment guide that covers everything from the basics of double materiality to the specifics of how to document and report on your findings.

2. Tackle key elements in the transition plan

The ESRS E1 requires businesses to provide a detailed account of their climate transition plan. In a nutshell, this is a corporate action plan to achieve net zero emissions by 2050.

The key elements of a climate transition plan include:

- Establishing science-based climate targets.

- Identifying and implementing decarbonization measures with quantifiable reduction goals.

- Securing financing for decarbonization initiatives.

- Embedding the transition plan in your overall business strategy and financial planning.

- Obtaining approval from the board.

- Aligning the plan with climate risk management and integrating into the governance framework.

3. Create an action plan guiding climate change

This action plan should detail the specific steps your business will take to combat climate change, including:

- Implementing sustainable practices across core operations: Whether it's reducing waste, improving energy efficiency, or sourcing sustainable materials, outline the practical and coordinated actions you plan to take.

- Stakeholder engagement: Describe how you will involve employees, customers, suppliers, and the wider community in your sustainability efforts.

4. Set clear goals for GHG reduction or removal

Your action plan should include specific, measurable goals for reducing GHG emissions in line with the Paris Agreement and the EU’s goal of climate neutrality by 2050. Consider setting science-based targets to ensure they are ambitious yet achievable.

5. Track and disclose total energy usage

Monitor and report on your total energy consumption (both renewable and non-renewable sources) for transparency and to identify areas for improvement.

6. Report GHG emissions across all three scopes

Under ESRS E1, businesses must follow the Greenhouse Gas (GHG) Protocol methodology and report on Scope 1, 2, and 3 emissions. These include:

- Scope 1: Direct emissions from owned or controlled sources.

- Scope 2: Indirect emissions from the generation of purchased energy.

- Scope 3: All other indirect emissions that occur in the value chain including both upstream and downstream business activities.

Select the right software for climate change reporting

If your business is set to report on CSRD, tackling the climate change topics under ESRS E1 can feel overwhelming and complex - especially for smaller teams coordinating across systems.

This is where the right tools can make all the difference.

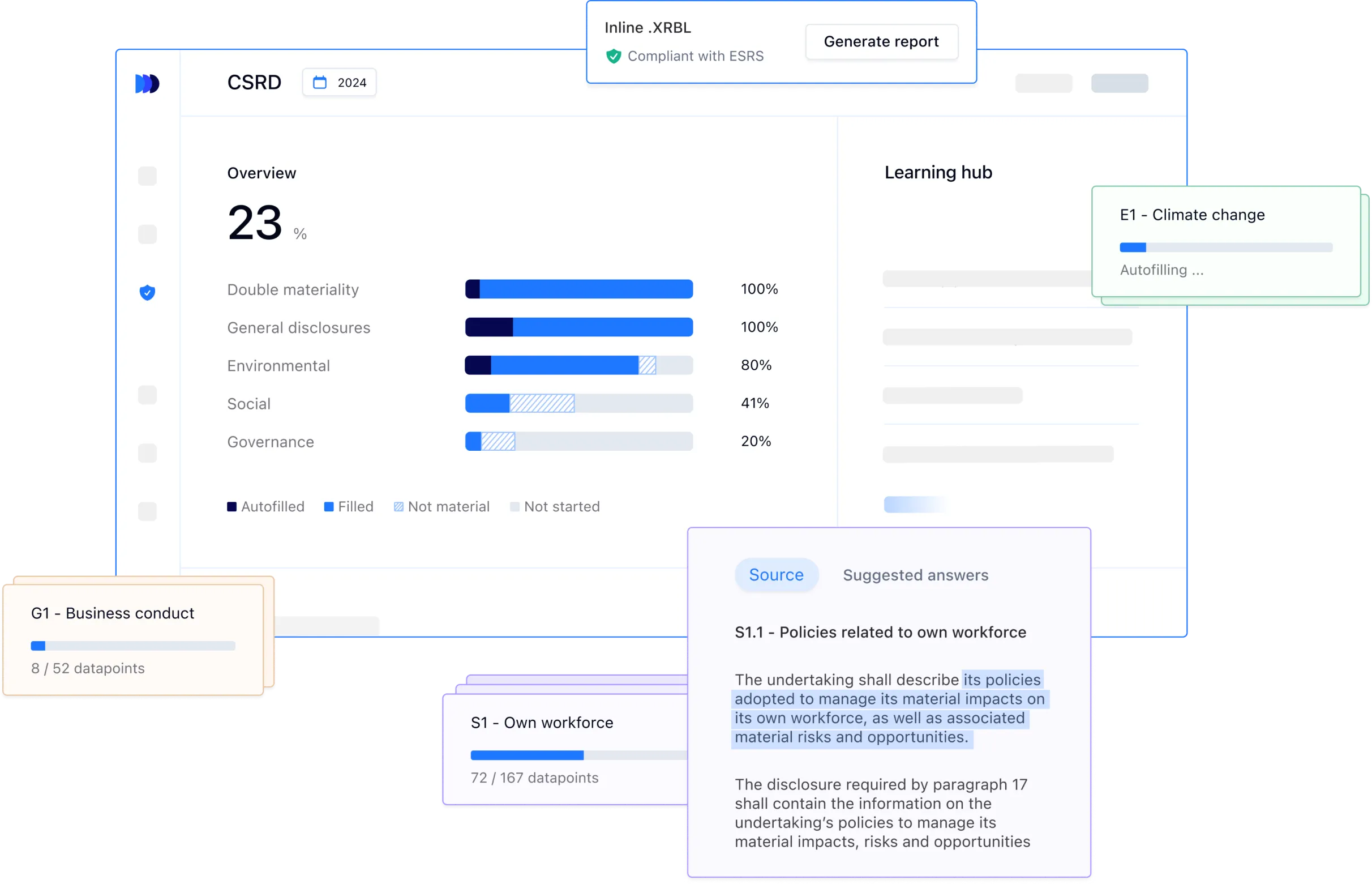

Climate change reporting software like Coolset is specifically designed to simplify the process for you and your team. It streamlines data collection and analysis, provides actionable reduction recommendations, and generates reports automatically to accelerate your compliance journey.

Discover how Coolset can fast-track your CSRD compliance by requesting a free demo today.

Practical guidance on building audit-proof evidence trails and internal controls while requirements are still evolving.

on mobile screens

to experience this demo.

↘ Check if your documentation meets PPWR requirements

This free compliance checker scans your packaging documentation and maps it against mandatory PPWR data requirements, giving you a clear view of your compliance status. Get actionable insights on documentation gaps before they become compliance issues.

Get your CSRD compliance suite

Streamline data collection and reporting across the Double Materiality Assessment and ESRS topic disclosures.

.webp)