ESRS E1 climate reporting: what changes under the amended ESRS (2026)

Disclaimer: New EUDR developments - December 2025

In November 2025, the European Parliament and Council backed key changes to the EU Deforestation Regulation (EUDR), including a 12‑month enforcement delay and simplified obligations based on company size and supply chain role.

Key changes proposed:

- New enforcement timeline: 30 December 2026 for large/medium operators, 30 June 2027 for small/micro operators

- Simplified DDS: One-time declarations for small and micro primary producers

- Narrowed scope: Most downstream actors and non‑SME traders would no longer need to submit DDSs

- New DDS requirement: Estimated annual quantity of regulated products must be included

These updates are not yet legally binding. A final text will be confirmed through trilogue negotiations and formal publication in the EU’s Official Journal. Until then, the current EUDR regulation and deadlines remain in force.

We continue to monitor developments and will update all guidance as the final law is adopted.

Key Takeaways

- The Amended ESRS E1 expands climate reporting from 9 to 11 disclosure requirements under CSRD, with the finalized standards expected to apply from January 1, 2027.

- EFRAG submitted the amended standards to the European Commission in November 2025; adoption as a delegated act is expected by mid-2026.

- Companies concluding climate change is not material must now explicitly justify that conclusion.

- Coolset helps companies collect emissions data, structure ESRS E1 disclosures, and generate CSRD-compliant reports automatically.

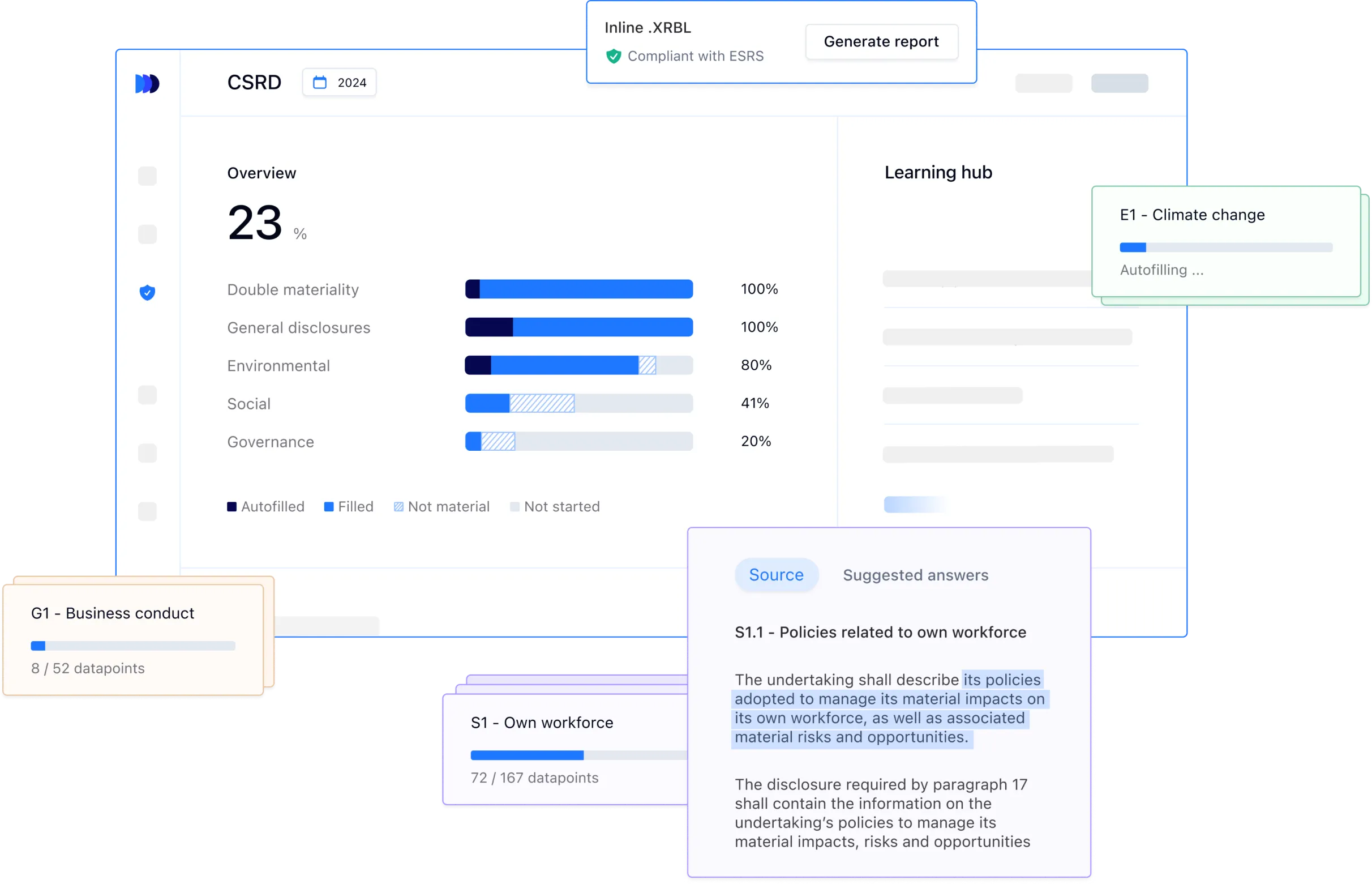

The Corporate Sustainability Reporting Directive (CSRD) has already transformed how large European companies approach sustainability reporting. At the heart of this transformation is ESRS E1 — the European Sustainability Reporting Standard on Climate Change. For most companies in scope, ESRS E1 will be among the most demanding standards to comply with, requiring detailed disclosures on emissions, targets, transition plans, and climate-related risks and opportunities.

This article explains what ESRS E1 requires, what changed under the Omnibus I Directive, and how companies should prepare.

What is ESRS E1?

ESRS E1 governs how companies report on their relationship with climate change. It covers:

- Governance and strategy for climate-related matters

- Transition plans and climate targets

- Scope 1, 2, and 3 GHG emissions

- Physical and transition climate risks and opportunities

- Energy consumption and efficiency

- Carbon removal and offsetting activities

The standard is structured around the concept of double materiality — companies must report on how climate affects them financially (financial materiality) and how their operations affect the climate (impact materiality).

What ESRS E1 requires: core disclosures

Transition plan (E1-1)

Companies must disclose their transition plan for climate change mitigation. This includes how the company’s business model aligns with limiting global warming to 1.5°C and achieving the EU’s 2050 climate neutrality objective. The transition plan must cover near, medium, and long-term milestones and how they are resourced and managed.

Emissions targets (E1-4)

Companies must disclose their climate-related targets, including GHG reduction targets. Targets should be specific, time-bound, and aligned with scientific pathways where possible. Science-Based Targets initiative (SBTi) alignment is increasingly the benchmark.

GHG emissions (E1-6)

This is the most data-intensive ESRS E1 requirement. Companies must disclose:

- Scope 1: Direct emissions from owned or controlled sources

- Scope 2: Indirect emissions from purchased electricity, heat, and steam (both location-based and market-based)

- Scope 3: All other indirect emissions across the value chain, covering all relevant categories

Scope 3 reporting is subject to a 3-year phase-in provision. However, companies should begin building their Scope 3 measurement infrastructure immediately, as this data is also required for other purposes (e.g., supplier engagement, SBTi target-setting).

Physical and transition risks (E1-9)

Companies must disclose the financial effects of climate-related risks and opportunities on their financial position and performance. This includes quantified impacts where possible, though quantification of financial effects has a 1-year phase-in.

What changed with Omnibus

The Omnibus I Directive introduced significant changes to ESRS E1. For companies now in scope (1,000+ employees and >€450M turnover), the key changes are:

- Mandatory data points in ESRS E1 reduced significantly

- Many previously mandatory disclosures moved to conditional or optional status

- Sector-specific ESRS for high-emitting sectors scrapped

- Simplification of transition plan requirements for smaller Wave 2 companies

For the full picture of what changed across all ESRS standards, see our guide to the amended ESRS.

How to prepare for ESRS E1 compliance

- Build your GHG inventory: ESRS E1-6 is the foundation. Start with Scope 1 and 2, then build toward Scope 3 coverage.

- Set science-based targets: E1-4 requires climate targets. SBTi-aligned targets are increasingly the market standard and satisfy ESRS requirements.

- Develop your transition plan: E1-1 requires more than a net-zero pledge — it requires a credible roadmap with milestones, resources, and governance.

- Assess climate risks and opportunities: Link TCFD-style analysis to your ESRS E1 financial risk disclosures.

- Build traceable documentation: Every E1 metric will go to limited assurance. Auditors need to trace each figure back to its source.

How Coolset supports ESRS E1

Coolset’s carbon accounting module provides TÜV Rheinland-certified Scope 1, 2, and 3 measurement aligned with the GHG Protocol and ESRS E1 requirements. The platform integrates GHG accounting directly with CSRD reporting, ensuring E1 disclosures are traceable, consistent, and audit-ready.

For more on the regulatory context driving ESRS E1 requirements, see our guide on the EU Omnibus proposal and what it means for CSRD scope. To see Coolset in action, book a demo.

Practical guidance on building audit-proof evidence trails and internal controls while requirements are still evolving.

on mobile screens

to experience this demo.

↘ Check if your documentation meets PPWR requirements

This free compliance checker scans your packaging documentation and maps it against mandatory PPWR data requirements, giving you a clear view of your compliance status. Get actionable insights on documentation gaps before they become compliance issues.

Get your CSRD compliance suite

Streamline data collection and reporting across the Double Materiality Assessment and ESRS topic disclosures.

.webp)