Navigating the VSME: a practical guide for mid-market companies

.webp)

Disclaimer: New EUDR developments - December 2025

In November 2025, the European Parliament and Council backed key changes to the EU Deforestation Regulation (EUDR), including a 12‑month enforcement delay and simplified obligations based on company size and supply chain role.

Key changes proposed:

- New enforcement timeline: 30 December 2026 for large/medium operators, 30 June 2027 for small/micro operators

- Simplified DDS: One-time declarations for small and micro primary producers

- Narrowed scope: Most downstream actors and non‑SME traders would no longer need to submit DDSs

- New DDS requirement: Estimated annual quantity of regulated products must be included

These updates are not yet legally binding. A final text will be confirmed through trilogue negotiations and formal publication in the EU’s Official Journal. Until then, the current EUDR regulation and deadlines remain in force.

We continue to monitor developments and will update all guidance as the final law is adopted.

Key takeaways

- The VSME is a voluntary ESG reporting standard developed by EFRAG, offering a proportional alternative to the CSRD for companies no longer in mandatory scope after the Omnibus changes.

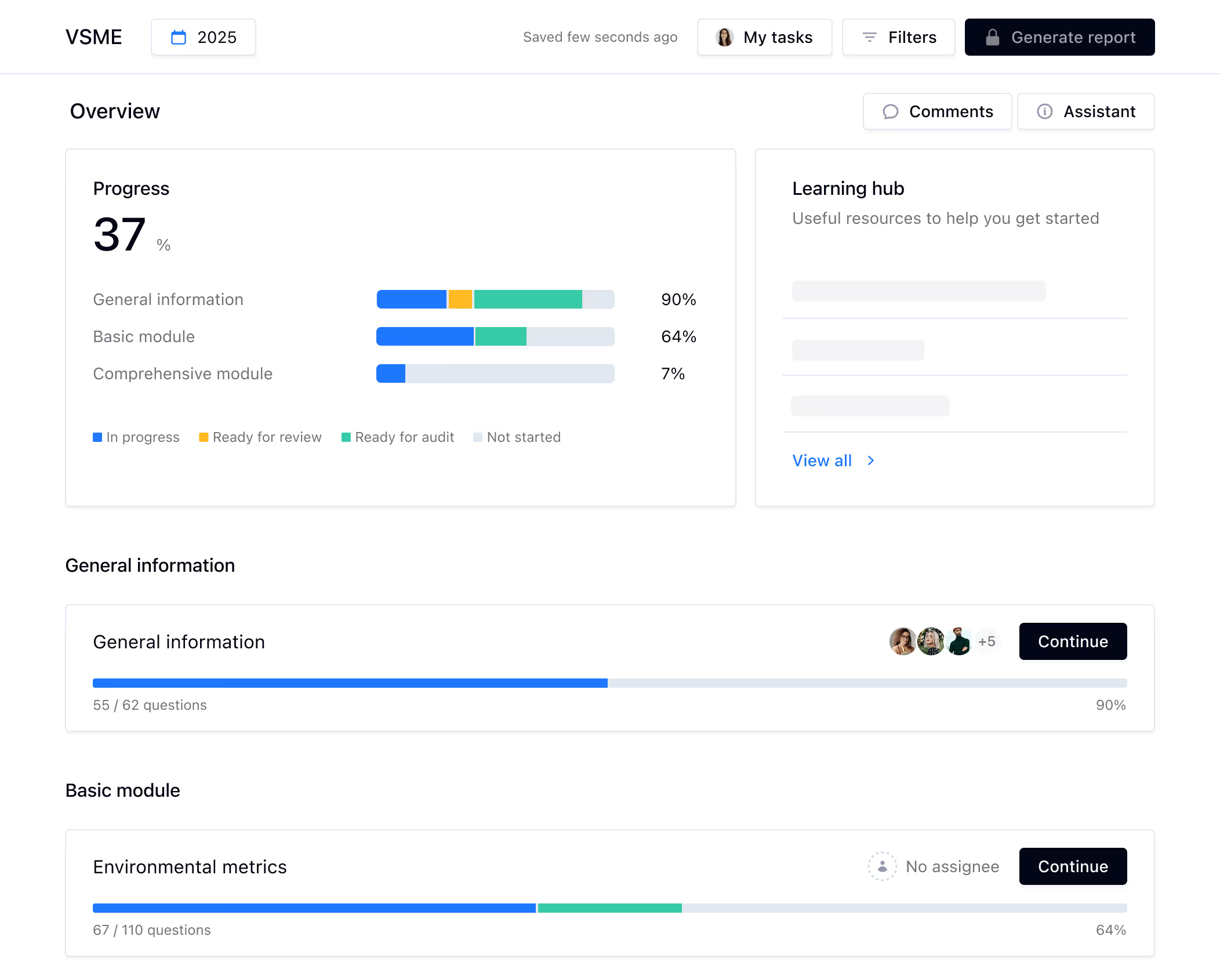

- The framework includes a Basic Module (~50 data points) and a Comprehensive Module (~100 data points), covering environmental, social and governance disclosures that banks, investors and supply chain partners increasingly expect.

- Coolset's VSME module guides teams through both modules with structured workflows and automated reporting.

The Omnibus proposal is set to change the ESG reporting landscape – as over 40.000 businesses that previously had to report on Corporate Sustainability Reporting Directive (CSRD) may no longer fall under its scope.

This comes at a time when thousands of companies have already put their ESG efforts in motion. If ever, now is the time to take advantage of the momentum and leverage the internal and external wins linked to ESG (like risk mapping, future-proofing and validating long-term strategies).

While industry leaders and investors alike agree that the European Union should halt its deregulation drive, companies are now looking for a working alternative. That’s where the sustainability reporting standard for non-listed micro, small and medium enterprises (VSME) comes in.

It’s a voluntary, streamlined ESG reporting framework. Even if you’re no longer legally required to report, ESG transparency remains a key competitive advantage as expectations from stakeholders continue to rise.

Why companies are still opting for structured ESG reporting

The Omnibus proposal is reshaping the ESG reporting landscape. With mandatory CSRD requirements loosening, thousands of companies now face a choice: stay the course with CSRD, transition to the VSME, or scale back ESG reporting altogether.

The first market signals are clear: most companies are sticking to structured reporting. Organizations competing on a European or global level recognize that a level playing field drives competitiveness. Between companies slightly above or below the CSRD threshold, those taking a proactive approach to sustainability will have the market advantage. With audit requirements removed, costs for CSRD alignment have come down, making it a logical choice for those already on track.

For companies that struggled with CSRD timelines or lacked the scale to support the full framework, VSME provides a right-sized alternative. The framework keeps the core principles of CSRD but removes unnecessary complexity. It signals maturity, reinforces credibility with banks and investors, and ensures a business remains aligned with evolving expectations from customers and partners.

Companies now fall into three categories:

- Mandatory CSRD – Companies with over 1,000 employees remain in scope and continue aligning with CSRD.

- Voluntary CSRD – Mid-sized companies committed to sustainability are staying on track, recognizing the competitive and financial benefits of CSRD alignment.

- VSME adoption – Smaller organizations looking for a practical, proportional reporting framework are transitioning to VSME.

Today, we’re diving into VSME — what it is, why it matters, and how it strengthens businesses both organizationally and competitively for the future.

What is the VSME standard?

The voluntary standard is a flexible and practical ESG reporting framework designed specifically for SMEs. Developed by EFRAG, the standard provides a proportional and simplified approach to sustainability reporting — aligned with the European Sustainability Reporting Standards (ESRS) of the CSRD but tailored to the needs and capabilities of smaller businesses.

The voluntary nature of the VSME standard makes it an ideal choice for companies that still want to measure, track, and report their ESG performance, even as the scope of mandatory CSRD requirements has been reduced under the Omnibus proposal.

Who should use the VSME standard?

The VSME standard is designed for any business that wants to track and report on ESG performance, regardless of whether they are legally required to do so. While originally developed for SMEs, the framework is now applicable and recommended to a broader range of companies that seek a practical, proportional, and voluntary approach to ESG reporting.

Your company should consider using the VSME standard if:

- You want to align with European ESG standards without unnecessary complexity – The VSME standard is built on the same principles as the ESRS but offers a more streamlined, business-friendly approach.

- You want to provide ESG data to key stakeholders – Banks, investors, and large business partners increasingly request sustainability data, even if you’re not legally obligated to report under CSRD.

- You’re part of a supply chain that prioritizes sustainability – Without ESG transparency, your company risks falling behind as more corporations integrate sustainability criteria into procurement decisions.

- You aim to future-proof your company – ESG reporting helps identify risks, optimize operations, and position your company for future regulatory developments.

- You need a structured yet flexible sustainability framework – Whether you’re new to ESG reporting or refining existing practices, the VSME standard allows for scalable implementation, letting businesses start with core disclosures and expand over time.

{{custom-cta}}

Understanding the VSME data points

The VSME framework offers two ESG reporting options: the Basic Module and the Comprehensive Module. The Basic Module covers core ESG metrics like energy use, emissions, workforce composition, and anti-corruption — ideal for a streamlined, proportional approach. The Comprehensive Module builds on this, adding disclosures on strategy, climate transition, human rights, and sector-specific data, making it suitable for businesses seeking greater transparency for investors and banks. Completion of the Basic Module is required before opting for the Comprehensive Module.

Good to know: The VSME incorporates many elements of the CSRD. Companies that have already completed a double materiality assessment under the ESRS and/or have gathered data for the ESRS data points, are very well positioned to report on the VSME standard. The most advanced tools can help streamline this transition by automatically mapping and prefilling progress across these interoperable frameworks — whether you’ve tracked your ESG data within or outside the software.

Basic Module: The compact ESG report

Best for: Companies looking for a lightweight but effective ESG report—ideal for businesses that want to meet stakeholder expectations without extensive reporting requirements.

The Basic Module includes around 50 data points that focus on essential ESG disclosures, covering the core aspects of sustainability performance. It is designed to be practical and proportional, ensuring that companies can comply without overburdening their operations.

What It covers:

General information:

- Business structure and legal form

- Sector classification (NACE codes)

- Workforce size and geographical operations

- Whether the report is individual (business-only) or consolidated (includes subsidiaries)

- Details of any sustainability-related certifications or labels

Environmental metrics:

- Energy use & greenhouse gas (GHG) emissions (excluding Scope 3):

- Total energy consumption (MWh)

- Breakdown by renewable vs. non-renewable sources

- Scope 1 emissions (direct emissions from company-owned sources)

- Scope 2 emissions (indirect emissions from purchased electricity, heat, or cooling)

- GHG intensity (emissions per euro of turnover)

- Pollution (if applicable):

- Only required if legally obligated or voluntarily monitored: Emissions to air, water, and soil

- Biodiversity impact:

- Number and area (in hectares) of business sites near biodiversity-sensitive areas

- Water management:

- Total water withdrawal

- For companies with water-intensive operations: Water use in high-stress areas

- Water consumption (difference between withdrawal and discharge)

- Resource use & circular economy:

- If applicable: Application of circular economy principles

- Waste generation (hazardous and non-hazardous)

- Percentage of waste recycled or reused

Social metrics:

- Workforce structure:

- Number of employees by contract type (permanent vs. temporary)

- Gender breakdown

- For companies with 50+ employees: Employee turnover rate, reported as the percentage of employees who leave the company during the reporting year

- Health & safety:

- Work-related accident rate

- Number of work-related fatalities

- Fair wages & workforce development:

- Whether employees earn at least the legal minimum wage

- Required for companies with 150+ employees, lowering to 100 in 2031: Gender pay gap

- Percentage of employees covered by collective bargaining agreements

- Average number of training hours per employee (broken down by gender)

Governance metrics:

- Anti-corruption & bribery compliance:

- Number of corruption or bribery convictions in the reporting period

- Total amount of fines incurred

Comprehensive Module: The complete ESG report

Best for: Companies that want to provide a detailed, investor-ready ESG report, particularly those seeking financing, investor confidence, or a strong sustainability profile for large corporate clients.

The Comprehensive Module contains around 100 data points (compared to 1.100 in CSRD), and expands on the Basic Module, adding more in-depth insights on sustainability strategy, risk management, and sector-specific ESG considerations.

What It adds:

Strategy & business model

- Key products/services and their sustainability impact

- Significant markets (B2B, B2C, wholesale, countries of operation)

- Operational business relationships

- If applicable: ESG-related elements in the company’s strategy

Environmental strategy & climate transition

- GHG reduction targets & climate transition plans:

- Scope 1 & Scope 2 emission reduction targets

- Scope 3 reporting

- Climate adaptation actions for identified climate risks

- Time horizons for climate-related risks (short, medium, long-term)

- For companies with significant environmental footprints: Detailed pollution & water impact reporting:

- Expanded reporting on air, water, and soil emissions

- More granular water consumption and wastewater discharge data

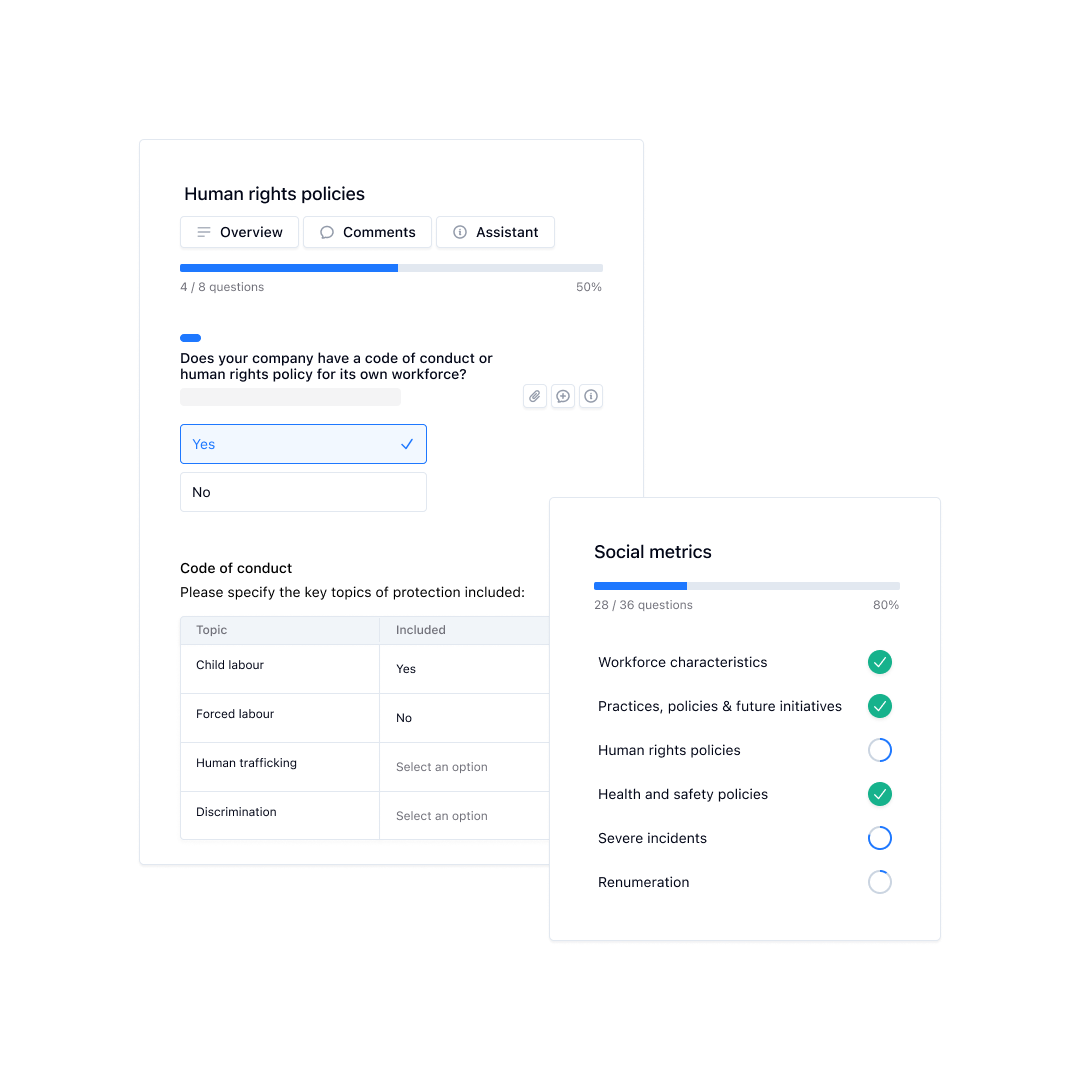

Social & human rights disclosures

- Diversity & inclusion:

- For companies with 50+ employees: Female-to-male ratio in management

- Breakdown of self-employed workers and temporary contract workers

- Human rights & labor practices:

- Code of conduct or human rights policy covering:

- Child labor

- Forced labor

- Human trafficking

- Discrimination

- Workplace safety

- Complaints-handling mechanisms for human rights violations

- Reporting on confirmed incidents of labor rights violations (own workforce and value chain)

- Code of conduct or human rights policy covering:

Governance & financial transparency

- Sector-specific ESG reporting:

- Revenues from controversial sectors (e.g., fossil fuels, weapons, tobacco)

- If applicable: Exclusion from EU reference benchmarks

- Corporate governance:

- Gender diversity in governance structures

.webp)

What’s next

Investors, banks, and large business partners still expect sustainability data, and having a structured ESG report helps you build trust, secure financing, and future-proof your organization. The VSME standard provides a manageable, actionable framework that allows businesses to report on ESG performance without excessive complexity.

To guide this process, Coolset has launched a dedicated and modular VSME module: starting with the Basic framework and extending into Comprehensive. It’s designed to streamline reporting while setting you up with an end-to-end sustainability management platform for both current and future ESG needs.

Want to learn more? Find a time with our team.

Learn how the new VSME framework helps mid-sized companies navigate ESG reporting after CSRD rollbacks.

on mobile screens

to experience this demo.

↘ Check if your documentation meets PPWR requirements

This free compliance checker scans your packaging documentation and maps it against mandatory PPWR data requirements, giving you a clear view of your compliance status. Get actionable insights on documentation gaps before they become compliance issues.

Start reporting on VSME

Collect ESG data, collaborate and create structured, automated reports with Coolset.

.webp)